One board spent 12 weeks preparing owners before the number became official. The other waited for a complete answer. Only one kept its owners’ trust.

Nearly three-quarters of U.S. community associations are underfunded compared with their own reserve needs, according to Association Reserves’ analysis of more than 100,000 reserve studies since 1986, representing all 50 states. Using 70% funded as its threshold, the firm reports that 74% of associations fall short.

The gap has widened in recent years: rising construction and material costs between 2021 and 2024 outpaced how quickly many associations adjusted their reserve contributions, a trend that Association Reserves* ties to inflation rather than to any single event.

That pattern is not new, and that is the point. Boards have had some version of this information for decades, yet the tendency to underfund is steadfast. The math did not change. What boards are now expected to do with the data they have has undergone a seismic shift.

Reserve funding was once treated as a discretionary budgeting decision, weighed against other priorities and revisited only when convenient, or faced head-on only by boards with the thickest skins. It is now squarely a fiduciary decision, carrying legal and regulatory consequences most boards have not yet reckoned with.

of associations studied fell below 70% funded.

Association Reserves* analysis of 100,000+ reserve studies, 1986–2025.

* Association Reserves’ dataset comprises associations that retained professional reserve-study providers and should therefore be interpreted as directional rather than statistically representative of every U.S. association.

Reserve studies have always been serious documents, whether their recommendations were followed, modified, or ignored. They matter because they create a contemporaneous record of what a board knew, when it knew it, and what information informed later decisions — evidence that goes directly to whether a board met its fiduciary obligations. The specific duty at issue is the duty of care.

Commissioning a reserve study alone does not satisfy that duty. The duty is to act on what the study shows, in proportion to the risk it describes.

Simply commissioning a study — regardless of whether it was read or adopted — substantially undermines any later claim that the board did not know about a deficiency. Once discovered, the study becomes the record of what the board was told, and every subsequent decision, including the decision to do nothing, is measured against that record.

Commissioning a study is not the same as discharging the duty.

That seriousness matters more today than it did 10 years ago. Cherry-picking reserve study recommendations without a documented rationale is much harder to defend. Instead, it is the exact fact pattern that turns a financial shortfall into a governance failure, and a governance failure into fiduciary exposure for the individuals who serve on the board — not just the association they represent.

None of that means a board must accept every recommendation uncritically. A board can question assumptions, commission an updated study, or phase a project. What a board cannot do, once it holds the study, is treat its recommendations as discretionary.

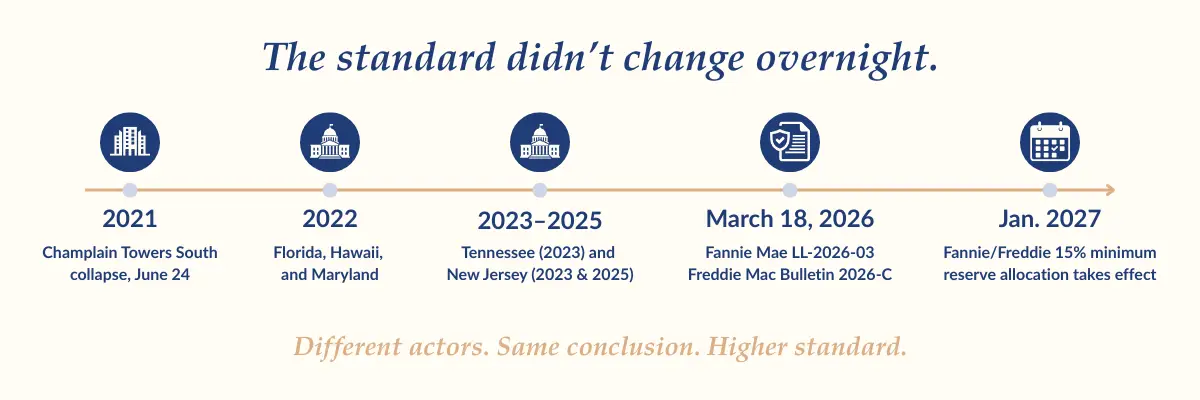

As the Association Reserves data shows, capital reserve underfunding began long before Champlain Towers South collapsed in Surfside, Florida, in June 2021. That tragedy exposed the worst case: the outcome boards could rationalize away, despite professional warnings to the contrary, as long as it stayed a hypothetical. The collapse made it a documented reality, and made a long-standing practice impossible to ignore.

The result is a new, more exacting standard against which a board’s knowledge is measured. That standard didn’t happen overnight. It took shape as investigators traced the causes of the collapse and the systemic gaps came into view.

In the years since, legislatures, lenders, insurers, and courts have each moved within their own authority to raise the bar for what a reasonable board is expected to understand and act on.

Boards today are expected to maintain a current reserve study, and it is their conduct after receiving that study — not merely commissioning one — that is measured against their fiduciary obligations to the association.

That is a substantially heavier standard than most boards realize they are being held to.

Boards change regularly, generally at least annually, through staggered service terms. Some changes are minimal; incumbents are reelected. Others rotate in new members. Some have held committee or other non-board service roles; others are doing community service for the first time.

New members often arrive with different assumptions about what the role requires, and many assume the job is rules, complaints, landscaping, and assessment levels. They may also bring known and unknown biases or agendas that affect board dynamics.

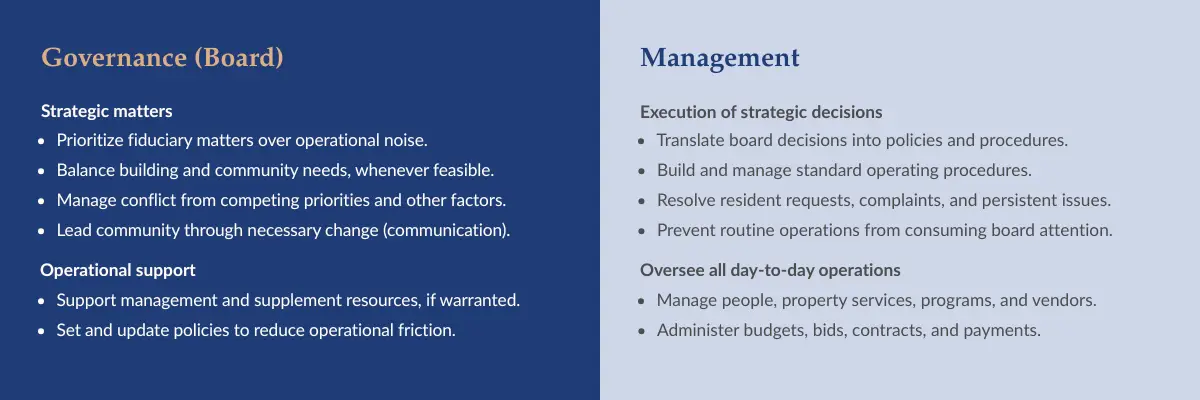

Those issues are real, and they command a disproportionate share of a board’s attention. Operational details, owner requests and complaints, and annual budgets are the visible parts of board service.

But, like an iceberg, there are far weightier decisions that boards must make — decisions that cannot be delegated — with much further-reaching effects than what’s visible beyond the conference room.

A single reserve decision can now affect whether owners can sell, whether buyers can get a conventional mortgage, how insurance underwrites the building, what the association must disclose, and whether an engineering recommendation becomes a manageable project or a special assessment.

A board member who is ignorant of those connections — or worse, does not think they matter — is not equipped to meet the duty the role now carries. That is why a single orientation meeting, a board packet, or an occasional reserve study presentation is not education.

Associations hire property managers, engineers, reserve specialists, attorneys, insurance brokers, accountants, contractors, and dozens of other professionals over the life of a building. Each brings expertise within a defined scope of practice. That specialization is appropriate. The problem begins when professional responsibility ends at the edge of that scope.

Volunteer boards carry the fiduciary duty for the association as a whole, but they rarely possess the technical expertise, time, or perspective needed to integrate every recommendation into a coherent plan. They depend on professionals to do more than complete individual assignments. They depend on those professionals to help them recognize what comes next.

Reserve studies, budgets, engineering reports, insurance coverage, capital planning, repair scheduling, and owner communication are no longer separate conversations. Decisions made in one area increasingly affect every other. Each specialty is an interdependent part of the same governance system.

And that system continues to evolve. In March 2026, Fannie Mae and Freddie Mac added mortgage eligibility more explicitly to that network of interdependencies, reinforcing that decisions once viewed as internal financial matters can now affect owners’ ability to buy, sell, and refinance.

That does not mean every adviser should become an expert outside their own profession. An engineer should not practice law. An attorney should not design structural repairs. An insurance broker should not write reserve studies. But each should recognize when the board is approaching the limits of its knowledge and help bring the appropriate expertise into the discussion.

An HVAC contractor replacing a failed fan might notice that a nearby fire-safety controller appears compromised. The contractor is not expected to diagnose the fire protection system. The professional response is to say, “This may be outside my scope, but I recommend having your fire-safety contractor look at this before we close the project.”

“This may be outside my scope, but I recommend having your fire-safety contractor look at this before we close the project.”

An engineer designing a repair might conclude that the adjacent structure warrants review by a structural specialist before construction begins. An insurance broker reviewing a renewal might recognize that the association’s reserve funding or deferred maintenance could create underwriting concerns and recommend involving the reserve specialist or the association’s attorney before the issue becomes a claim.

This is not about expanding anyone’s scope of practice. Some professionals already work this way, and certain disciplines — attorneys and accountants, for example — are accustomed to making referrals as part of their practice.

The opportunity is for this mindset to become more common across the full range of professionals who advise community associations.

Professional responsibility includes helping clients understand where one discipline ends and when another is needed, and helping to bring the right expertise to the table.

That level of coordination should not be viewed as exceptional service. As community associations become more complex, boards will increasingly judge professional advice not only by technical accuracy within a discipline, but by whether it helps them make better decisions across the system as a whole.

Every hour spent relitigating a minor enforcement dispute is an hour not spent on reserve funding, structural integrity, or owner communication. That isn’t a time-management problem. It’s a fiduciary duty: a board can’t discharge its duty to the whole association if its attention is consumed by persistent nuisances rather than the matters that affect every owner’s shared assets.

Good governance means building systems — a rules committee, clearer manager authority, disciplined agendas — so operational noise doesn’t crowd out structural obligations. Responsible boards don’t dismiss owner concerns. They build systems so those concerns get heard and resolved through existing policy, or escalated for a documented board decision — one that’s then communicated and enforced consistently.

It’s also disrespectful to the entire community when substantive matters like reserve funding, structural integrity, mortgage eligibility, and owner communications persistently receive short shrift because 12 versions of the same infraction have consumed far more board time than they warrant, in the name of making sure “the board weighs in” and “every owner gets equal time.”

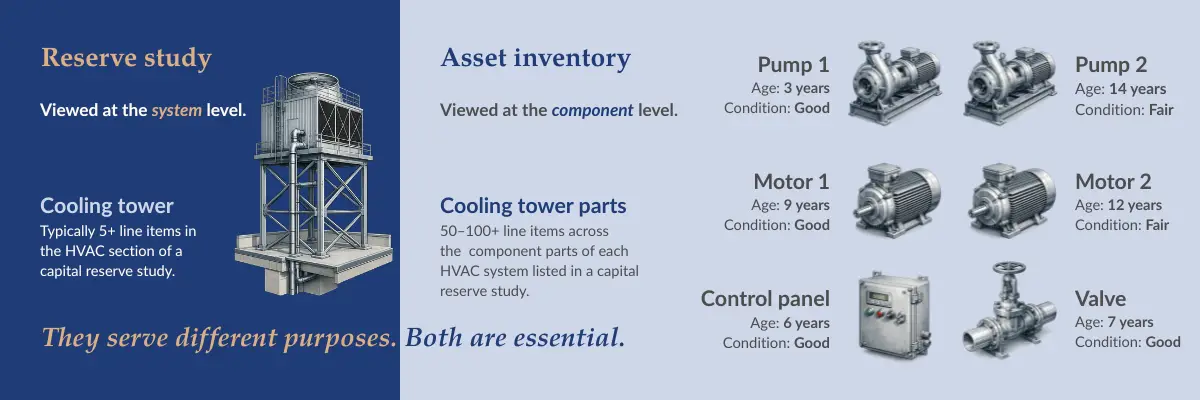

In layman’s terms, a reserve study treats a cooling tower as a component in the larger HVAC system. The section on cooling towers may only break down a handful of items: the structural steel dunnage; fan and motor; chiller, condensers, or evaporators; air inlet louvers; and the water distribution system.

That’s because capital reserve studies are financial planning tools. They’re used to plan large-scale projects, often the full replacement of certain systems. Collecting details down to individual parts consumes time, which translates into higher professional service costs. That makes sense from a budgeting, finance, and capital planning perspective.

From a day-to-day perspective and from a board perspective, details matter. If one of the five pumps in a cooling tower’s water distribution system fails on a blazing-hot Friday in August, the board has no option but to approve an unplanned $25,000 expense.

Instead of scrambling to get a quorum of board members on the phone to approve the repair, an asset inventory shows that pump 2A is past its useful life. With the authority the board has already granted, the property manager can authorize the repair, inform the board president, and add an agenda item to the next meeting to ratify the expense.

An asset inventory does not remove the fiduciary duty to act wisely. It provides the board and management with the information necessary to fulfill those duties responsibly and with the least operational friction.

Mae and Freddie Mac carry so much weight in this conversation, even though they have no regulatory authority over associations.

Fannie Mae and Freddie Mac moved together on persistent reserve underfunding, and the timing wasn’t a coincidence: Lender Letter LL-2026-03 and Freddie Mac’s Bulletin 2026-C, both issued March 18, 2026, tie reserve funding, reserve studies, and baseline-funding practices directly to condominium project eligibility. Beginning January 4, 2027, the minimum replacement reserve allocation increases to 15%, from 10%, of a project’s annual budgeted assessment income. As of August 3, 2026, reserve study budgets can no longer rely on baseline funding.

A project that falls outside these standards does not necessarily lose all buyers, but the pool of conventional buyers shrinks, refinancing gets harder, and owners often discover the problem mid-transaction. In practice, a lender’s questionnaire effectively serves as a recurring third-party audit of whether the board met its duty, whether anyone intended it that way or not.

March 18, 2026

Lender Letter LL-2026-03 and Freddie Mac Bulletin 2026-C tie reserve funding, reserve studies, and baseline-funding practices directly to condominium project eligibility.

August 3, 2026

Reserve study budgets can no longer rely on baseline funding, a strategy that allows reserves to approach, but not fall below, zero.

January 4, 2027

The minimum replacement reserve allocation increases from 10% to 15% of a project’s annual budgeted assessment income.

Florida’s SB 4-D is the clearest direct response to Champlain Towers South: it created mandatory milestone inspections and structural integrity reserve studies for buildings three stories and higher, and now prohibits associations from waiving reserve funding for those components. New Jersey and Tennessee acted on similar timelines, each requiring boards to commission reserve studies and act on their findings — in New Jersey’s case, adopting a funding plan once a study reveals a shortfall.

Maryland’s statewide reserve-study requirement traces further back to a task force convened in 2005; the version that finally passed in 2022 had failed in three prior legislative sessions and became law the same year as the collapse of Champlain Towers South. Hawaii’s disclosure requirements arrived the same year, on their own track.

The triggers differ. The direction doesn’t: reserve funding, inspection, and disclosure are increasingly treated as governance obligations rather than discretionary financial choices. Boards should confirm current requirements with counsel in their own jurisdiction.

States have responded in different ways. Some now require structural inspections, some require reserve studies or funding plans, and some have adopted both. The table below illustrates how approaches continue to evolve.

| Jurisdiction | Structural Inspection Required | Reserve Funding Required | Notes |

|---|---|---|---|

| Florida | Yes — milestone inspection, buildings 3+ stories | Yes — SIRS, non-waivable | Most comprehensive framework; hard 365-day repair deadline |

| New Jersey | Yes — covered buildings, load-bearing systems | Yes — CAI National Reserve Study Standards; 30-year funding plan | Flexible funding options with owner disclosure requirements |

| Maryland | No | Yes — statewide reserve study | Reserve funding required, no inspection mandate |

| Tennessee | No | Yes — reserve study, annual review | Reserve funding only, no inspection mandate |

| Hawaii | No | Yes — 30-year reserve projection | Disclosure-focused; no inspection mandate |

Regardless of how, a board that meets its fiduciary obligations today sets aside time for reserves, insurance, and structural integrity, rather than letting enforcement disputes consume every meeting. It has a reserve study that gets read and acted on, not filed. It has an asset inventory that turns emergency repairs into documented, ratified decisions. It brings advisers together rather than letting each stay in their own lane. And it tells owners what it knows before the number is final, not after.

That is not extra work layered onto board service. That is what board service now requires.

Volunteer board members are not expected to become engineers, attorneys, reserve specialists, or lenders. They are expected to govern responsibly in a world where those professions increasingly intersect. The board’s responsibility is no longer to know everything. It is to recognize when expertise is needed, ask better questions, integrate the advice it receives, and make decisions that reflect the duty it owes the association.

Costs change. Conditions are discovered that no prior inspection caught. No reserve plan removes uncertainty entirely, and an assessment born from a genuine surprise is not, by itself, evidence of poor governance.

The failure is a board that knew, through a reserve study it commissioned, and said nothing until the bill came due. That is where fiduciary questions begin: not the expense, but the silence about a risk the board was already on notice of.

A board that says, early,

“We updated our capital reserve study, as we’re required to do, and several items we’ve been watching need to be addressed. The total cost will likely exceed $X, but we are securing competitive bids now. That amount may change, but it’s the most accurate estimate we can give you right now.

“We will show you more concrete plans as soon as we have bids, and we plan to keep you updated throughout the process.

“We realize this is your home and are committed to keeping you informed about our shared assets,” is not attempting to make the assessment popular. It is discharging the duty to disclose what it knows, when it knows it, instead of when it becomes unavoidable.

A long-range financial planning document covering major common elements: components, remaining useful life, replacement cost, and recommended annual funding.

The operational record beneath the reserve study. A reserve study may list a cooling tower. An asset inventory lists the individual pumps, motors, valves, and controls within it, along with their ages, maintenance histories, and conditions.

What the association should have accumulated if owners had contributed proportionally toward the future repair or replacement of common elements over time.

Actual reserve balance measured against the fully funded balance, expressed as a percentage. Association Reserves classifies associations below 70% funded as underfunded.

A contribution strategy that keeps reserves close to the fully funded balance.

A contribution strategy that maintains reserves above a predetermined minimum funded level throughout the reserve study projection period.

A contribution strategy that allows reserves to approach, but not fall below, zero. It leaves little margin for cost changes and is increasingly incompatible with current lending standards. It is sometimes referred to as “$0 floor.”

A charge to association members (owners) outside the regular budget to fund an expense that the current reserve account balance cannot cover. It is not inherently a sign of poor governance. It becomes one after years of predictable, undisclosed underfunding.

No. Schedules vary by jurisdiction. Some use building age, others height, construction type, or location. Boards should confirm with their legal counsel or local Community Associations Institute (CAI) chapter which law applies to them, rather than assuming requirements are uniform nationwide.

Not necessarily. Reports often recommend prioritizing and phasing repairs, and boards retain judgment over sequencing. What boards cannot do is ignore documented structural findings because the repairs are expensive or unpopular. Florida sets a hard deadline — required repairs must commence within 365 days of a milestone inspection — and even where no statute sets a clock, the duty of care does

No. They answer different questions. An inspection evaluates the building’s condition; a reserve study evaluates how the association will fund repair and replacement. The strongest communities treat them as two halves of one process.

It happens more often than boards expect, and it isn’t a reason to default to inaction. An engineer may flag a component as urgent based on its physical condition; a reserve specialist may be working from a funding timeline that assumes a longer runway. When that happens, the board’s job is to bring both professionals into the same conversation rather than choosing one opinion over the other in a vacuum — the disagreement itself is often the most useful information the board receives, because it usually means the assumptions behind the funding plan need to be updated, not that either professional is wrong.

That depends on state law, and the trend is against it. Florida now prohibits waiving or reducing reserves for SIRS components. New Jersey requires associations to remedy funding deficits on a statutory timeline. Owner reluctance does not override a board’s duty on structural findings. Boards should confirm with counsel in their jurisdiction how that principle applies to non-structural items bundled within the same report.

That is common — and being underfunded is not, by itself, evidence of poor governance. Ignoring the finding after it has been documented is the problem. The goal is a realistic funding strategy that is adopted and communicated before the shortfall becomes an emergency.

Because reserve funding and structural condition have become proxies for building risk. In March 2026, Fannie Mae and Freddie Mac announced updated guidelines tying reserve funding, reserve studies, and repair history directly to condominium project eligibility, with the stricter reserve threshold taking effect in January 2027, which means a board’s structural decisions now affect owners’ ability to sell and refinance. That subject has its own companion pillar.

Structural integrity is not just an engineering issue; it is a leadership issue. The strongest communities do not wait for a crisis to force difficult conversations. They build systems that identify risk early, communicate it clearly, and turn expert advice into coordinated action — which is precisely what The Well-Run Building exists to help boards do.

If your board is navigating structural inspections, reserve funding, or changing lending requirements, explore the companion pillars on reserve funding and mortgage eligibility, or schedule a conversation to talk through where your building stands today.

Structural integrity is one part of a larger governance challenge. Reserve funding, mortgage eligibility, and the systems boards use to turn professional advice into decisions are increasingly connected.

Continue with long-form articles on reserve funding, special assessments, mortgage eligibility, and the decisions facing condominium and community association boards.

The Well-Run Building is a free program to help condo, co-op, and HOA boards explain structural integrity, reserve funding, and mortgage eligibility before crisis communication are needed.

Board Consulting helps boards clarify decisions, responsibilities, priorities, and the systems needed to move difficult work forward.

You don’t need to have the answer before we talk.